Last Updated on July 20, 2020 by John Prendergast

Growing a financial advisory business for scratch is hard. It takes long hours and persistence.

Creating a high growth advisory business is even harder. It takes new thinking and outstanding execution to create a service that is much better at meeting client needs than alternatives.

Here’s how one high growth advisor created his rocket ship.

Jason Wenk’s story.

Jason opened his first Retirement Wealth Advisors office in Michigan in 2005. He focused on baby boomers and retirees using seminar marketing.

The firm grew quickly.

Fast forward to 2010, Jason had added two employees and opened his first satellite office.

Sounds perfect right? But, there was a problem.

Growth began to slow as scaling was difficult to achieve serving only local clients.

But, like a lot of financial advisors, Jason is an overachiever.

The backstory.

At 19, Jason started his career as the youngest of more than 50,000 Morgan Stanley employees, building software for advisors to use internally.

After years of working 80-hour weeks in their back office, he decided he could deliver advisory services at least as well as the people he was supporting. So he left and began to build the framework for Retirement Wealth Advisors, his SEC registered RIA.

A high growth mindset.

Missing his growth goals wasn’t an option. But the growth and service approach Jason used when his business was small had become too time-consuming to continue.

He could continue on his current path and grow incrementally by offering slightly better services than the competition, using old-school marketing, and waiting for referrals.

Or he could radically rethink his business. He could remove every part that was limiting him and replace it with new tools that could help him grow exponentially.

Open minds see open opportunity.

He started by envisioning a firm where, rather than focusing on the local market, he could attract and support clients nationally. By removing geography as a limit, Jason dramatically increased the size of his potential market and his firm’s growth potential.

It also meant he could be more focused on the kinds of clients he wanted to work with. One additional benefit of thinking nationally was that his firm could pursue many growth strategies that weren’t feasible at the local level.

It began to work.

However, the strategy created a new challenge.

Jason had to develop a new service model that could support a national client base. In-person meetings becoming more and more challenging. He realized he had to either open offices all over the country and staff them or find a more centralized way of serving clients remotely.

He also needed to eliminate every process that clients didn’t actually value and focus on doing the few things that clients cared about. Most importantly, he wanted to be better at delivering those services than local competition. For Jason, that meant leveraging his background in technology to find a solution.

He needed a swiss army knife, not a fork

Jason knew he’d need to focus on a few key areas for clients.

1. Service experience

He believed he could actually improve the service experience by improving client meetings. He knew he could make them more focused and eliminate the need to travel by conducting virtual meetings.

To do it, he’d need a very simple web conferencing solution that was easy for clients to use.

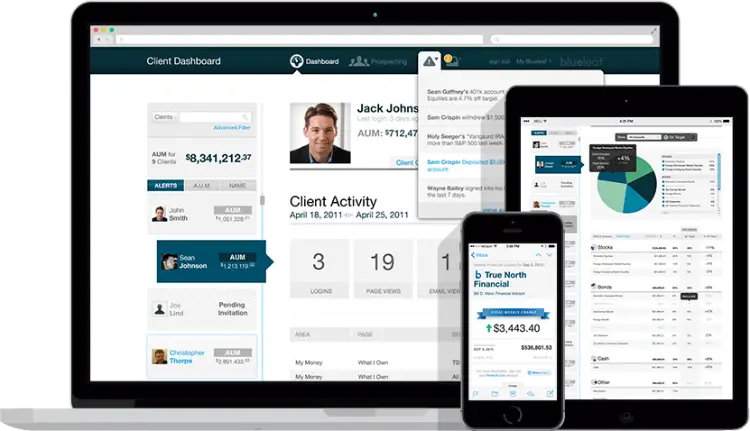

He would also need a client portal that allowed his staff to walk clients through their situation in a simple, easy to understand format that was automatically up-to-date. In addition to focused meetings, using a live portal would eliminate hours of meeting prep time for his staff.

Client onboarding would become simpler and more automated too. But, most importantly, it would let clients see all their assets in one place from anywhere.

A client portal would also allow Jason to eliminate the traditional, quarterly reports in favor of on-demand information and an automated system of relevant client contact.

The goal was better, more convenient service for more clients. His strategy was not either more clients or better service, it was more clients AND better service.

2. Self-service

Jason knew he’d need to be able to service everything that the client owned even if it wasn’t in his custody. By allowing clients to add all of their accounts into the portal he could give better advice, and eventually those assets were likely to move to him based on his ability to service them before anyone else.

That meant self-service account aggregation.

With a client portal and account aggregation, Jason didn’t want to get caught in the trap of having his staff maintain held-away accounts in a separate system and he didn’t want to be in the position of middleman if accounts needed to be maintained. Clients would need to be able to add their held-away accounts and ideally other accounts like bank accounts, credit cards and insurance.

By allowing clients to login to the portal anytime they had a question he also hoped to reduce the number of support calls since his clients would be able to answer a lot of those questions on their own whenever they wanted.

3. Communications

Jason is a big believer in the importance of regular client communications. In fact, he reaches out to his clients between 120-150 times per year. Jason realized that he need to automate at least some of these communications while delivering a highly personalized experience.

Jason meets Blueleaf.

Simplicity, transparency and a service breakthrough.

Jason first stumbled on Blueleaf’s financial relationship management platform in September of 2011 in an Investment News article. After doing a little research, he became an early adopter because he believed in the Blueleaf vision of simplicity for advisors and clients.

Jason started introducing Blueleaf to his clients.

“They loved it.”

“In the past, I’d used a lot of client portals and had never gotten a single compliment on any of them. This is the first system where I regularly get compliments, phone calls and emails that make me blush.”

“And because it’s an automated communication system, Blueleaf is a referral generating machine. Clients love it, and they tell their friends about it. I also use their prospecting tools to court new clients. Once prospects see it they want it.”

“With any business, but especially a virtual business, it is important to regularly communicate with your clients,”

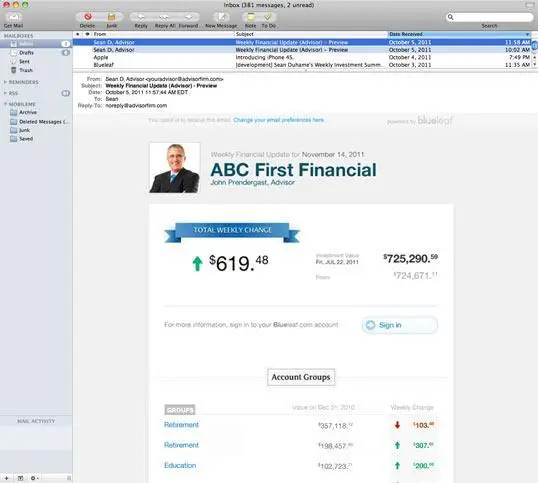

“Blueleaf sends out a weekly automated email update which includes my name, my picture and the name my firm. Think about it, that equates to 52 automated client touches per year with exactly what the client wants to know: ‘what do I have? & how am I doing?’

“Try it and you will find it’s incredibly helpful in establishing relationships with clients.”

Blueleaf “makes my life easier by gathering all of clients’ assets in one place. Anyone who has used most of the larger aggregation services is probably familiar with how complicated their portals are. Blueleaf is the opposite. It is also immensely helpful to really know where all their assets are, how they’re allocated, and how they’re performing. Identifying external accounts is now an integral part of my onboarding process.”

As an added bonus, Blueleaf also integrates with the other systems that Jason uses (like Wealthbox) to eliminate the need to manually re-enter data and manage multiple connections for each software system.

Clear blue sky ahead.

For the last 2 years, Jason has focused on building a virtual advisory where almost everything is done online.This change has allowed him to shift his focus from local clients to offer his services nationwide.

His cost to acquire clients is a fraction of what it used to be and he can be more specific about the type of client he wants to work with since the market is so much bigger now.

The growth rate is higher than it’s ever been and his practice is scalable which allows him to grow much more efficiently.

Retirement Wealth Advisors now has $1.3 B in AUM and over 5,500 clients.

Jason attributes a lot of his success to technology, especially Blueleaf.

“I would encourage anyone who is interested in building a business that is largely virtual to try Blueleaf. It’s a world-class technology that is changing the world of wealth management.”

Not a Blueleaf user?

Sign up for the trial and test the platform with a couple of clients. The trial is free.

Enjoy the time savings Blueleaf offers.

See your clients’ excitement when they log into Blueleaf and get their complete financial picture in one easy-to-understand view.

Receive their praise when they start getting their weekly emails.

Use Blueleaf with prospects to increase your close rate.

Discover new assets as clients add ALL their assets to the system.

For your free trial of Blueleaf, sign up here.